Estimated reading time: 11 mins

Dealing with overwhelming debt can feel like a never-ending battle. The constant stress of juggling multiple loan and credit card payments while still trying to afford basic living expenses is emotionally and financially draining. With interest charges and late fees continuously piling up, it often seems impossible to make any real progress in reducing what you owe.

If this describes your current financial situation, you’re not alone. Millions of Americans are trapped in cycles of high-interest debt without a clear path to repayment. But there are solutions available to help relieve your debt burden so you can regain control of your finances. Debt relief programs provide a lifeline of hope for a brighter, debt-free future.

The Mechanics of Debt Relief: A Path to Financial Freedom

To start moving towards financial freedom, it’s important to understand how debt relief programs actually work to reduce what you owe. The most common types of debt relief services include:

Debt Management Plans: A debt management plan consolidates your unsecured debts, like

credit cards and medical bills, into one monthly payment. The program negotiates with creditors to lower interest rates and get late fees waived. This makes monthly payments and your total repayment period more affordable.

Debt Settlement: Debt settlement companies negotiate directly with creditors to settle your debts for an amount less than what you originally owed. Most settlements save you 40 to 60% of the total balance. The program sets aside funds monthly in a dedicated account until enough is saved to make settlement offers.

Bankruptcy: Filing for bankruptcy is a legal means to address overwhelming debt. It involves a federal court process that either discharges debts entirely, allowing a fresh start or restructures debts into a manageable repayment plan over time.

This process provides relief by either liquidating assets to pay creditors or creating a plan that fits the debtor’s financial capacity, without specifying the exact chapters. Individuals must seek advice from financial or legal professionals to navigate the complexities of bankruptcy and determine the most suitable path based on their unique financial situations.

In the U.S., particularly in states such as California, individuals and businesses often encounter challenges with managing and overcoming debt. Creating a comprehensive overview of total debt enables strategic prioritization and management of obligations tailored to a company’s specific circumstances and objectives. It provides clarity on where relief efforts should be focused to rebalance the books and propel growth. Guidance and support from experts are crucial in navigating these issues, as they offer tailored advice and practical solutions to achieve financial stability.

High interest rates on credit cards and loans can escalate manageable debt into overwhelming burdens, forcing tough decisions about paying bills or affording necessities, and impacting mental health. However, there is hope for those struggling with debt. Consultation with debt relief experts offers a pathway to overcoming financial distress.

Like many other states, California has seen its share of residents facing financial hardship. With the economic impacts of the pandemic, many Californians have struggled with job losses, medical bills, and other debt that has become unmanageable. Specifically, debt relief programs in California play a significant role in assisting individuals and businesses to overcome their financial burdens. The journey to financial freedom is challenging, but with expert guidance, achieving financial stability is within reach for Californians struggling with debt.

Qualifying for Debt Relief: A Beacon of Hope

Wondering if a debt relief program is right for you? The good news is most programs have flexible eligibility requirements designed to provide real solutions for your financial situation.

Here are some common criteria to qualify:

- Total unsecured debt over $10,000

- Facing hardship making minimum payments

- Experiencing financial stress from debt burden

- Willingness to commit to the debt relief program

If the debt has taken over your finances and you need help, chances are good you’ll qualify for relief. Professional advisors offer free consultations to discuss your specific circumstances and debt totals to determine the best path forward.

There are no hard credit score requirements. Get the process started and discover the hope and support a debt relief program can provide.

The Advantages of Enrolling in Debt Relief Programs

The benefits of professional debt relief extend far beyond just reducing what you owe. Here are some of the key advantages enrolling can offer:

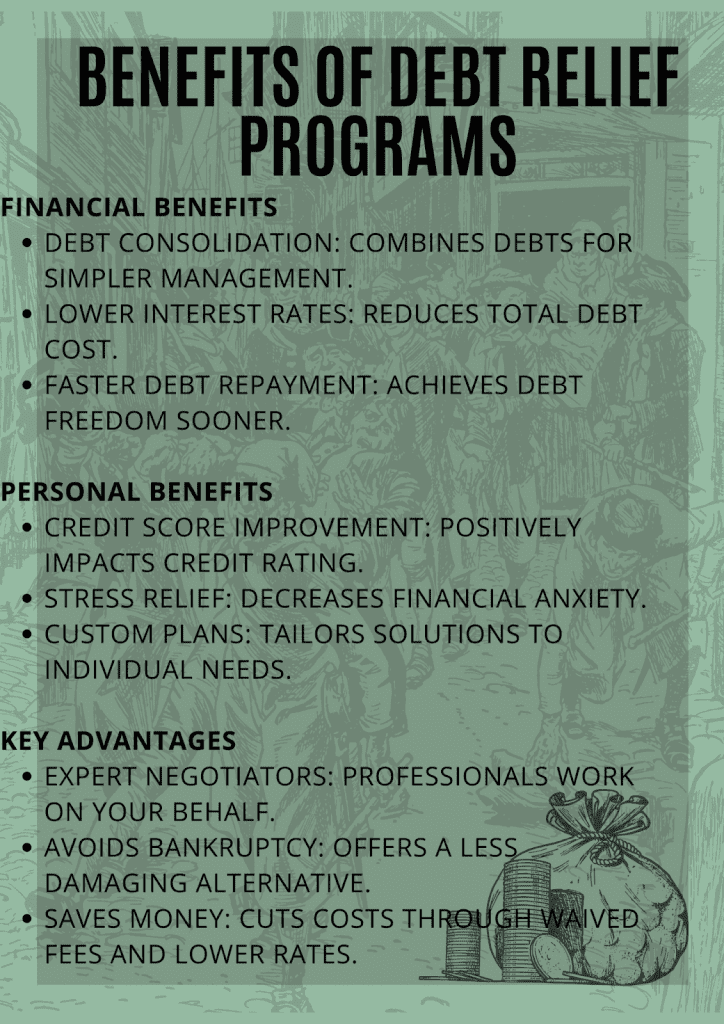

Lower Interest Rates

By consolidating debt, relief programs can negotiate much lower interest rates with your creditors, reducing the amount you pay in interest charges. This makes more of your payment go towards paying down the principal.

Lower Monthly Payments

Debt relief services work with you to create an affordable monthly payment plan based on your budget. This tailored payment is often 40-50% less than what you currently pay each month across multiple accounts.

Pay Off Debt Faster

With more affordable payments and lower interest rates, you can pay off your debt in 2-4 years through a debt management program – far faster than trying to do it alone.

Save Money Overall

Between reduced interest fees, lower monthly payments, and waived late fees, enrolling in debt relief ends up saving you thousands of dollars compared to staying on your current debt repayment path.

Tax Benefits

For qualified medical debt, credit card, and other unsecured debt settlements over $600 may be reported as taxable income. However, debt forgiven through bankruptcy is not taxable.

Improved Credit Score

As balances get paid down, your credit utilization rate drops, allowing your credit score to start improving. Completing a program responsibly can boost your score by up to 50-100 points.

Emotional Relief

Perhaps most importantly, professional guidance lifts the emotional weight of debt off your shoulders so you can focus on your mental health and look ahead to the future.

Tapping into this multitude of financial and personal benefits creates a silver lining to overcome the challenges of debt through a structured debt relief program.

Positive Impact on Financial Well-Being

While simply enrolling in debt relief brings immediate benefits, the true long-term impact can redefine your financial outlook and stability. Here are some of the life-changing effects debt relief programs can have:

- Renewed confidence in money management skills

- Relief from calls and letters from creditors

- Ability to start saving money each month

- Reduced financial stress and improved mental health

- Motivation to stick to a budget going forward

- Hope to qualify for future credit at better rates

- Blueprint for establishing an emergency fund

- Increased disposable income each month

- Peace of mind from becoming debt-free

These positive outcomes go beyond just eliminating debt to fundamentally improve your relationship with money. With new capabilities and motivation, you’ll be empowered to make financial decisions to enrich your life.

Strategies for Maximizing the Benefits of Debt Relief Programs

Once enrolled in a debt relief initiative, putting these strategies into practice will help you maximize the benefits:

- Stay committed to making your new monthly payment – This maintains trust and progress with creditors.

- Make lifestyle adjustments to live within your reduced budget – This might mean cutting discretionary spending on wants rather than needs.

- Don’t take on new debt – Avoid putting yourself deeper in the hole and delaying your debt-free goal.

- Leverage educational resources – Take advantage of financial counseling tools offered to build new money management skills.

- Communicate regularly with your program advisor – Keep them updated on any changes to your income or expenses so they can properly advise you.

- Automate payments – This reduces the chance of human error leading to missed payments.

- Track your progress – Watching debt balances go down month-to-month will keep you motivated.

Following this game plan will empower you to fully capitalize on debt relief programs as catalysts to achieve lasting financial health.

Navigating the Process with Confidence and Support

Embarking on the debt relief process requires courage and know-how. Here is expert guidance to equip you with the confidence, understanding, and assistance needed to smoothly navigate your debt-free journey:

Choosing the Right Debt Relief Program

Select an established, reputable company that’s right for your goals – whether that’s a debt management plan, debt settlement, or bankruptcy. They should have a strong track record of results and positive reviews.

Knowing What to Expect

From document collection to settlement negotiations to payment tracking, your advisor will outline what’s needed from you for each step of the process.

Getting Help from the Start

Enrolling provides immediate access to financial counselors who offer judgment-free support and advice as you begin.

Understanding It Takes Time

Remain patient and committed throughout the duration. Setbacks are normal. Debt relief is a process, not a quick fix.

Leveraging Available Resources

Quality programs provide tools like budgeting templates, educational courses, and customized advice to set you up for success.

With the benefit of experienced guidance and compassion, you can approach your debt relief plan with the self-assurance that a brighter future lies ahead.

Building a Debt-Free Future: Planning and Persistence

As the finish line of becoming debt-free nears through your relief program, it’s time to blueprint your financially liberated future. Careful planning and persistence now can make all the difference:

Set Realistic Financial Goals

Define specific, achievable targets – like building a 3-month emergency fund or qualifying for a mortgage. Your advisor can help strategize around your objectives.

Create a Monthly Household Budget

A detailed, well-researched budget allows you to maximize savings and work towards financial goals post-debt relief.

Build an Emergency Savings Fund

Experts recommend having 3-6 months of living expenses set aside for unexpected expenses. This provides a buffer that keeps you from having to take on new debt.

Invest for the Future

Explore low-risk investment opportunities like 401k or index funds to steadily build wealth over time.

Continue Monitoring Your Credit

Keep tabs on your score and report to ensure no new inaccurate information appears that could negatively impact you.

Persist in Your New Money Habits

Sticking to the lessons and practices you’ve cultivated will be vital for safeguarding your financial freedom. Old habits have allure, so remain vigilant.

With focus and determination, you can make your debt-free status the launching pad to the prosperous financial life you deserve.

Conclusion: A Brighter Financial Future Awaits

Life with overwhelming high-interest debt can feel bleak and hopeless if tackled alone. But professional debt relief programs shine a light leading out of the darkness. These services don’t just provide financial mechanisms to reduce your debt – they empower you to take control, relieve anxiety, and look ahead to a stable, debt-free life.

With an understanding of how programs work to your benefit, confidence in the qualifications and advantages, and strategies to maximize results – the way forward is illuminated. By embarking on the process with support and perseverance, you will emerge on the other side revitalized with new financial capabilities and freedom.

Debt relief can be challenging, but the payoff in peace of mind and economic mobility is life-changing. You now have the insights needed to take the next step and a community ready to help. A brighter financial future awaits – start your debt relief journey today.

FAQs

1. What are debt relief programs?

Debt relief programs are services designed to help individuals manage, reduce, or eliminate their debt. These programs work by negotiating with creditors to lower interest rates, reduce the total debt amount, or consolidate multiple debts into a single, manageable payment, providing a structured path toward financial stability.

2. How do debt relief programs work?

Debt relief programs start with a thorough assessment of your financial situation, including income, debts, and expenses. Based on this evaluation, a debt relief advisor will recommend a strategy tailored to your needs, such as debt consolidation, settlement, or a debt management plan. The aim is to make your debt more manageable or reduce it significantly.

3. Who qualifies for debt relief programs?

Qualification for debt relief programs typically depends on the amount and type of debt, financial stability, and the ability to make regular payments under the program. Most programs target individuals with unsecured debt, like credit card debt or medical bills, who are struggling to make minimum payments.

4. Are debt relief programs the same as filing for bankruptcy?

No, debt relief programs are not the same as filing for bankruptcy. These programs aim to reduce or manage debt without the severe financial implications of bankruptcy. Bankruptcy can offer a fresh start but comes with significant consequences for your credit score and ability to borrow in the future.

5. How long do debt relief programs take?

The duration of a debt relief program varies based on the amount of debt and the specific strategy employed. Some programs may take a few months to negotiate, while others, like debt management plans, can last from three to five years, depending on the agreed-upon payment schedules.

6. Will joining a debt relief program affect my credit score?

Participation in a debt relief program may impact your credit score initially, especially if it involves stopping payments to creditors as part of a debt settlement strategy. However, the long-term effect can be positive as you reduce your debt and improve your payment history.

7. How do I choose a reputable debt relief program?

Research is key to finding a reputable debt relief program. Look for programs with positive reviews, accreditation by organizations like the National Foundation for Credit Counseling (NFCC) or the American Fair Credit Council (AFCC), and transparency about fees and program requirements. Avoid any service that promises unrealistic results or charges fees before providing help.